Chapter 19 Shrinkage Methods

Reference: Ch6 in An introduction to Statistical Leraning with applications in R by James, Witten, Hastie and Tibshirani.

An introduction to glmnet: https://glmnet.stanford.edu/articles/glmnet.html

For theory behind the methods, study Statistical Learning I and II (STAT462, STAT457).

Packages used: glmnet, ISLR2

Introduction:

Regularization (or shrinkage) involves fitting a model where the estimated parameters are shrunken towards zero. The aim is to reduce overfitting and improve prediction accuracy.

Depending on the regularization method, some of the parameters may be estimated to be exactly zero (which thus improve model interpretability). Hence, regularization methods can also perform variable selection.

Variable selection here means the process of determining which variables to be included in your model. Examples that we have seen before are the forward stepwise regression, backward stepwise regression and the best subset selection.

Regularization is not limited to linear regression models (although we describe this idea using linear regression in this chpater). It is a general method that is also used in other methods as well (e.g., logistic regression, deep learning)

19.1 Ridge Regression

In linear regression, we minimize \[\begin{equation*} \sum^n_{i=1} \bigg( y_i -\beta_0 - \sum^p_{j=1} \beta_j x_{ij} \bigg)^2. \end{equation*}\] In ridge regression, we minimize \[\begin{equation*} \sum^n_{i=1} \bigg( y_i -\beta_0 - \sum^p_{j=1} \beta_j x_{ij} \bigg)^2 + \lambda \sum^p_{j=1} \beta^2_j, \end{equation*}\] where \(\lambda \geq 0\) is a tuning parameter to be determined separately.

The term \(\lambda \sum_j \beta^2_j\) is called a shrinkage penalty. This penalty is small when \(\beta_j\)’s are close to \(0\). Thus, it has the effect of shrinking the estimates of \(\beta_j\) towards \(0\).

\(\lambda\) is a tuning parameter that serves to control the relative impact of the shrinkage penalty.

For each value of \(\lambda\), there is a corresponding minimizer \(\hat{\beta}^R_\lambda\) of the loss function above in the ridge regression.

Note that we do not shrink the intercept \(\beta_0\).

Some properties of ridge regression:

Efficient to compute

Work also when \(p > n\). That is, when the number of covariates is greater than the sample size (least squares does not work in this case)

Does not select a particular model (i.e., include all \(p\) predictors in the final model)

Ridge regression usually performs better than the least squares because of the bias-variance trade-off. As \(\lambda\) increases, the bias increases but variance decreases.

Ridge regression works best in situations where the least squares estimates have high variance

19.2 LASSO

The lasso coefficients \(\hat{\beta}^L_\lambda\) minimize the quantity

\[\begin{equation*} \sum^n_{i=1} \bigg( y_i -\beta_0 - \sum^p_{j=1} \beta_j x_{ij} \bigg)^2 + \lambda \sum^p_{j=1} |\beta_j|. \end{equation*}\]

Recall the \(l_1\) norm of the vector \(\beta\) is given by \(||\beta||_1 = \sum^p_{j=1}|\beta_j|\). The lasso penalty \(\lambda \sum^p_{i=1}|\beta_j|\) is an \(l_1\) penalty.

The ridge penalty is an \(l_2\) penalty.

As with ridge regression, the lasso shrinks the coefficient estiamtes towards \(0\). However, the \(l_1\) penalty has the effect of forcing some of the coefficient estimates to be exactly equal to \(0\).

Hence, the lasso can be used to perform variable selection. Model generated from the lasso is easier to inerpret than those generated from ridge regression because of this.

A sparse model is a model that only involves a fraction of all the variables. Thus, lasso yields sparse models.

19.3 Selecting the tuning parameter

A standard way to choose the tuning parameter \(\lambda\) is to use cross-validation.

Steps:

Choose a grid of \(\lambda\) values

Compute the cross-vlidation error for each value of \(\lambda\)

Select the tuning parameter value for which the cross-validation error is smallest

Refit the model using all of the data and the selected value of the tuning parameter

19.4 glmnet

To perform ridge regression and the lasso in R, we can use the glmnet package. The main function in this package is glmnet(). In this case of linear regression, glmnet() solves the problem

\[\begin{equation*}

\min_{\beta_0, \beta} \frac{1}{n} \sum^n_{i=1} (y_i - \beta_0 - x^T_i \beta)^2 + \lambda\{

(1-\alpha) ||\beta||^2_2/2 + \alpha ||\beta||_1 \}.

\end{equation*}\]

This penalty is called the elastic net penalty. When \(\alpha = 0\), it becomes the ridge penalty. When \(\alpha = 1\), it becomes the lasso penalty.

We will illustrate how to perform ridge regression and lasso using Hitters data set from the package ISLR2. The data set contains \(322\) observations of major league players. The aim is to predict the salary of the player using other information about the players.

The syntax of glmnet() is different from lm() or glm(). In particular, we have to provide the x and y separately in the function.

In general, a data set may have some categorical variables. We can prepare the data set to be used in glmnet() using model.matrix().

The data set contains three factors: League, Division, NewLeague:

library(ISLR2)

# first remove rows with missing values

Hitters <- na.omit(Hitters)

head(Hitters[, c("League", "Division", "NewLeague")])

## League Division NewLeague

## -Alan Ashby N W N

## -Alvin Davis A W A

## -Andre Dawson N E N

## -Andres Galarraga N E N

## -Alfredo Griffin A W A

## -Al Newman N E AUse model.matrix to prepare the data. The first column is the intercept and we remove it when putting into glmnet().

x <- model.matrix(Salary ~., Hitters)[, -1]

y <- Hitters$Salary

head(x[, c("LeagueN", "DivisionW", "NewLeagueN")])

## LeagueN DivisionW NewLeagueN

## -Alan Ashby 1 1 1

## -Alvin Davis 0 1 0

## -Andre Dawson 1 0 1

## -Andres Galarraga 1 0 1

## -Alfredo Griffin 0 1 0

## -Al Newman 1 0 0Generate random indexes to split the data into training and testing data:

19.4.1 Ridge Regression

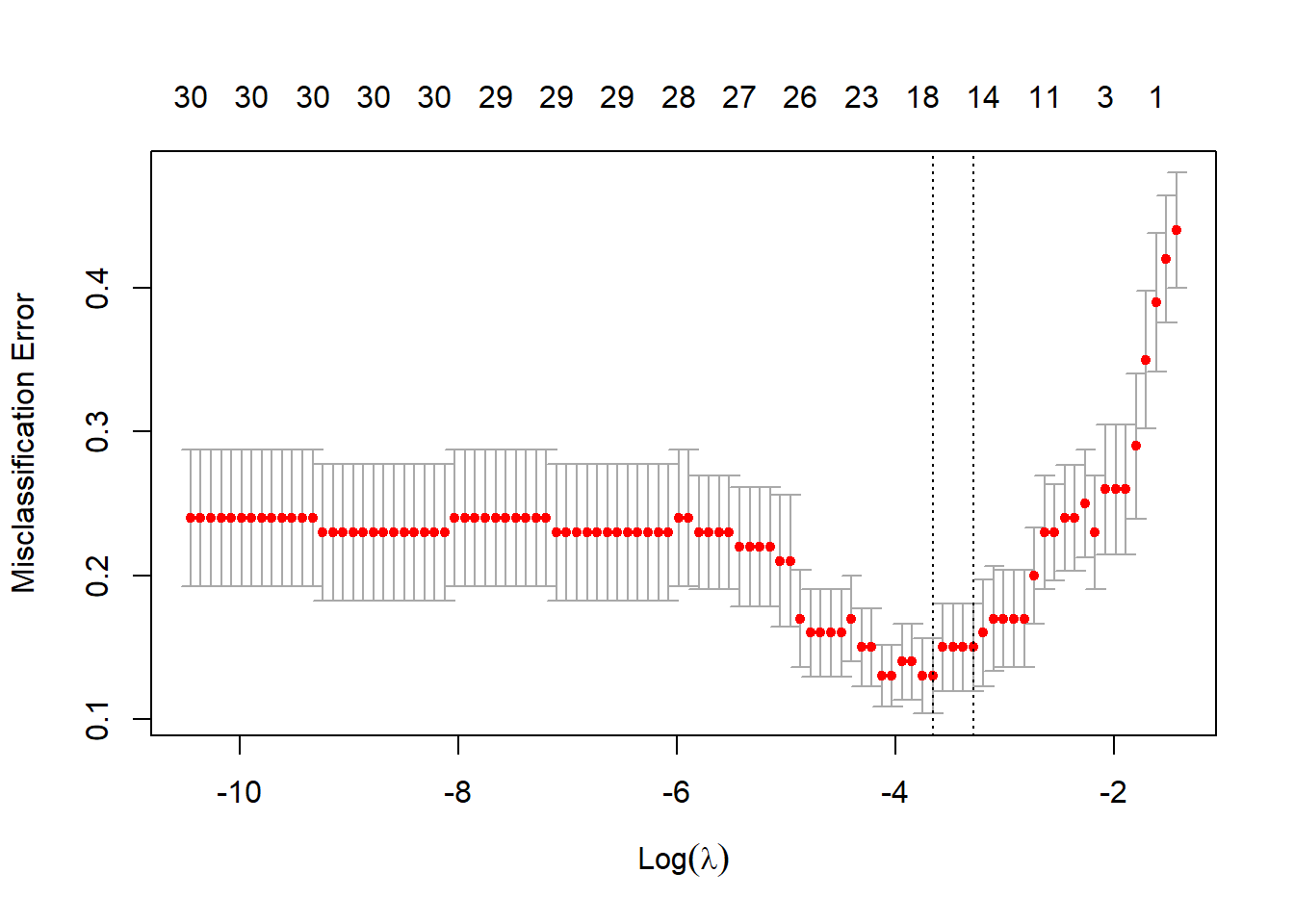

Perform ridge regression with cross-validation. The default option is \(10\)-fold CV. Note that by default, the variables will be scaled automatically in the function.

The above plot shows the cross-validation error (the mean squared error computed using the CV approach) with different values of \(\lambda\) in the \(\ln\) scale. We can pick the \(\lambda\) that results in the smallest cross-validation error using the following code:

Fit the ridge regression for the training data set with the “best” lambda and evaluate the test error.

# ridge regression with a particular value of lambda

ridge_best <- glmnet(x[index, ], y[index], alpha = 0, lambda = best_lambda)

# form predictions

ridge_pred <- predict(ridge_best, s = best_lambda, newx = x[-index, ])

# test error

mean((ridge_pred - y[-index])^2)

## [1] 138800.2Coefficients (when the variables are in the original scale):

predict(ridge_best, type = "coefficients")[1:ncol(x), ]

## (Intercept) AtBat Hits HmRun Runs RBI

## 71.16411532 0.05151174 0.31495026 2.49638228 0.68833226 0.73836757

## Walks Years CAtBat CHits CHmRun CRuns

## 1.77444807 -0.48852879 0.01327951 0.06333713 0.62913292 0.12448162

## CRBI CWalks LeagueN DivisionW PutOuts Assists

## 0.15070839 0.16896589 31.16003691 -77.93859127 0.09125514 0.06393766

## Errors

## -0.33532271Compare with the least squares approach

ls_fit <- lm(Salary ~ ., data = Hitters[index, ])

ls_pred <- predict(ls_fit, Hitters[-index, ])

mean((ls_pred - y[-index])^2)

## [1] 168593.3We can see that the test error obtained from ridge regression is smaller.

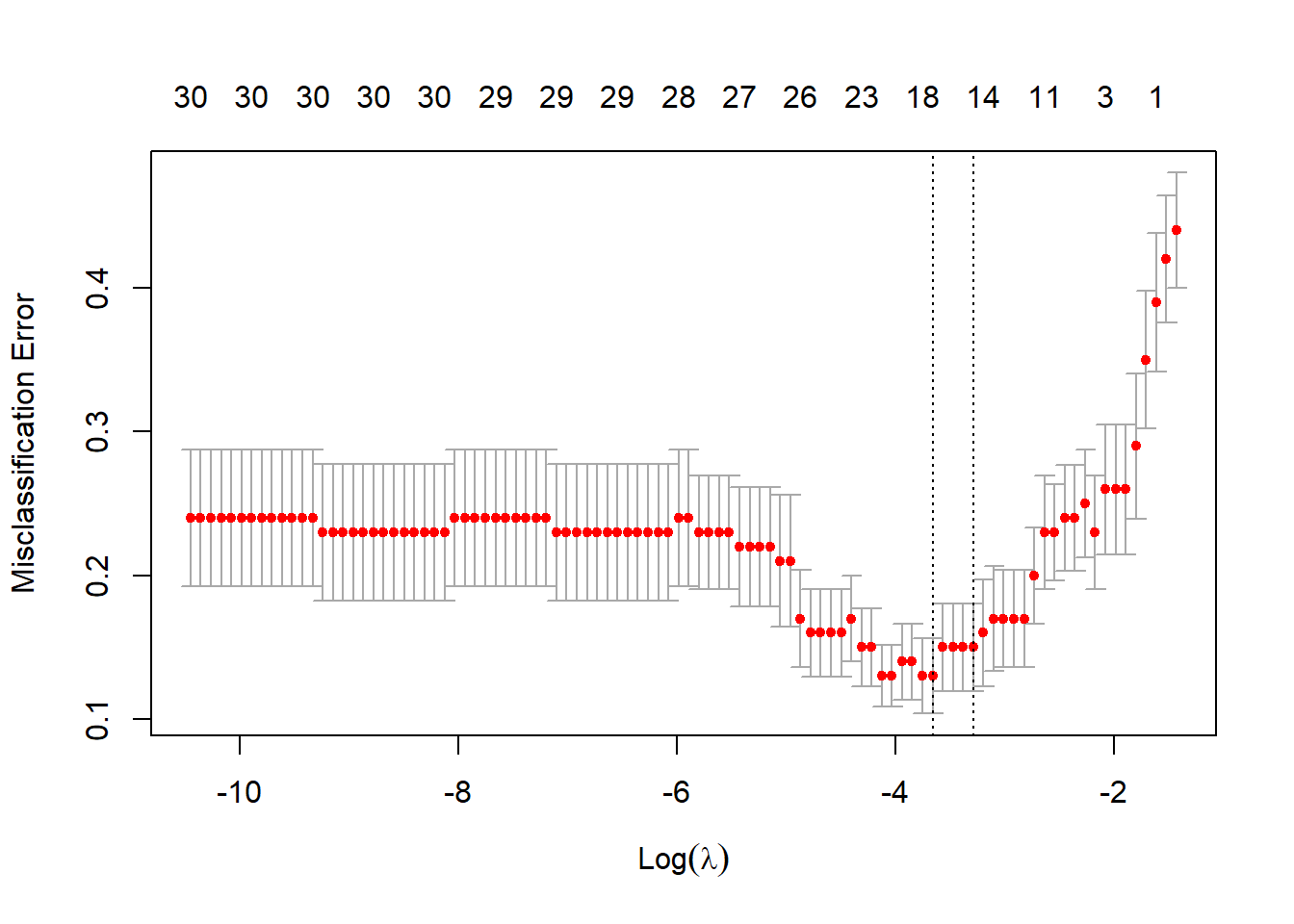

19.4.2 LASSO

The code to perform LASSO is essentially the same as that in ridge regression. We only need to change the value of alpha to 1.

# find the best lambda

best_lambda <- lasso_cv$lambda.min

lasso_best <- glmnet(x[index, ], y[index], alpha = 1, lambda = best_lambda)

# form predictions

lasso_pred <- predict(lasso_best, s = best_lambda, newx = x[-index, ])

# test error

mean((lasso_pred - y[-index])^2)

## [1] 144127.2The test error obtained from lasso is also smaller than that obtained from the least squares approach.

Coefficients (when the variables are in the original scale):

predict(lasso_best, type = "coefficients")[1:ncol(x), ]

## (Intercept) AtBat Hits HmRun Runs

## 126.13087838 0.00000000 0.00000000 3.49595499 0.00000000

## RBI Walks Years CAtBat CHits

## 0.00000000 3.93919763 -15.95901778 0.00000000 0.23935217

## CHmRun CRuns CRBI CWalks LeagueN

## 0.87111840 0.00000000 0.39819654 0.00000000 52.95398929

## DivisionW PutOuts Assists Errors

## -139.60281921 0.12169771 0.14858018 -0.06371655We can see that the lasso results in a model where the coefficient estimates are sparse: \(7\) of the estimates are exactly \(0\).

Variable selection property of LASSO

In the following toy example, the response is only related to the first five features \(X_1,\ldots,X_5\): \[\begin{equation*} Y_i = 1 + 3(X_{i1} + \ldots +X_{i5}) + \varepsilon_i \end{equation*}\] We apply LASSO and see that LASSO can select the true model, that is, a linear model that only includes \(X_1,\ldots,X_5\).

set.seed(2)

x <- matrix(rnorm(500 * 20), nrow = 500, ncol = 20)

y <- 1 + rowSums(x[, 1:5]) * 3 + rnorm(500, 0, 0.1)

# Perform CV to find the best lambda

lasso_cv <- cv.glmnet(x, y, alpha = 1)

best_lambda <- lasso_cv$lambda.min

# Refit the data with the best lambda

lasso_best <- glmnet(x, y, lambda = best_lambda, alpha = 1)

# Estimated regression coefficients

predict(lasso_best, type = "coefficients")[, 1]

## (Intercept) V1 V2 V3 V4 V5

## 1.023367 2.926722 2.912596 2.917734 2.928092 2.921180

## V6 V7 V8 V9 V10 V11

## 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000

## V12 V13 V14 V15 V16 V17

## 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000

## V18 V19 V20

## 0.000000 0.000000 0.00000019.5 Penalized Logistic Regression

Let \(y_i = 1\) or \(0\) be the response.

The objective function for penalized logistic regression is: \[\begin{equation*} \min_{(\beta_0, \beta)\in\mathbb{R}^p } \left\{ -\left[ \frac{1}{n}\sum^n_{i=1} \left( y_i (\beta_0 + \beta^\top x_i) - \log (1+e^{\beta_0 + \beta^\top x_i })\right) \right] + \lambda \left[\frac{1-\alpha}{2} \|\beta\|^2_2 + \alpha\|\beta\|_1 \right] \right\}. \end{equation*}\]

We can obtain the estimates using glmnet():

Perform CV to choose \(\lambda\):

There are different measures for “error”:

classgives misclassification erroraucgives area under the ROC curve

19.6 Penalized Multinomial Regression

Response: \(G_i \in \{1,\ldots,K\}\). Let \(y_{ik} = 1, y_{ij} = 0\), \(j\neq k\) if \(G_i= k\).

The objective function is \[\begin{equation*} -\frac{1}{n}\sum^n_{i=1} \left[ \sum^K_{k=1}y_{ik}(\beta_{k0} + \beta^\top_k x_i) - \log \sum^K_{k=1} e^{\beta_{k0} + \beta^\top_k x_i} \right] + \lambda \sum^K_{k=1}\|\beta_k\|_1. \end{equation*}\] where we do not penalize the intercept.

Getting the MNIST dataset

library(dslabs)

mnist <- read_mnist()

i <- 5

image(1:28, 1:28, matrix(mnist$test$images[i,], nrow = 28)[ , 28:1],

col = gray(seq(0, 1, 0.05)), xlab = "", ylab="")

library(glmnet)

train_X <- mnist$train$images

train_y <- mnist$train$labels

test_X <- mnist$test$images

test_y <- mnist$test$labels

# subset a smaller dataset for illustration

set.seed(1)

subset <- sample(1:nrow(train_X), 1000, replace = FALSE)

cvfit <- cv.glmnet(train_X[subset, ], train_y[subset], family = "multinomial", parellel = TRUE)

pred <- predict(cvfit, newx = test_X, s = "lambda.min", type = "class")

table(pred, test_y)

## test_y

## pred 0 1 2 3 4 5 6 7 8 9

## 0 930 0 19 8 2 22 21 9 17 23

## 1 1 1096 28 7 5 7 14 23 39 9

## 2 7 2 844 24 5 5 17 22 3 6

## 3 0 10 33 784 4 32 21 11 32 11

## 4 2 1 23 1 883 20 22 13 25 63

## 5 20 5 4 90 4 728 42 3 76 22

## 6 8 3 24 11 10 11 812 1 15 1

## 7 8 0 16 28 8 18 2 858 16 60

## 8 4 18 37 32 7 32 7 10 724 5

## 9 0 0 4 25 54 17 0 78 27 809

# misclassification rate

sum(pred != test_y) / length(test_y)

## [1] 0.1532